If you wish to avoid common errors in financial reporting assignments, then read the instructions carefully, follow the right accounting standards, keep the data organized, review entries, and check your calculations. Also, manage time properly and practice regularly to complete assignments successfully and build a strong foundation for a career in finance.

Financial reporting is an important part of business operations because it gives a clear view of a company’s financial health and performance. If you are a finance student or a professional, then when you work on financial reporting assignments, you should make sure to maintain accuracy. Committing mistakes while preparing financial reports is common, but they can affect your grades as well as your understanding of real-world financial decisions. So, it is crucial to avoid certain mistakes in financial reporting assignments. Do you wonder how to prepare error-free financial reporting assignments? If so, read this blog. Here, we have discussed what financial reporting is, why errors happen, the mistakes you might make in financial reporting assignments, and how you can avoid them.

What is Financial Reporting?

Financial reporting is the process of creating reports that show a company’s financial activities over a certain period. These reports, such as the balance sheet, income statement, cash flow statement, and statement of changes in equity, help you understand a company’s financial health. Both people inside the company, like managers and employees, and people outside, like investors, regulators, and lenders, use these reports to make important decisions.

The main goal of financial reporting is to be clear and transparent. It ensures that all financial information is presented fairly and consistently as per the recognized accounting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). In academic settings, financial reporting assignments will test your ability to follow these rules, interpret financial data, and present it in an organized way.

Why Do Financial Reporting Errors Happen?

Mistakes in financial reporting assignments happen more often than you might think, even if you understand accounting principles well. Usually, knowing why these errors occur can help you avoid them and improve the accuracy of your work. Some common reasons include

- Many students confuse concepts such as accruals and deferrals, revenue recognition, or depreciation methods, which can lead to incorrect figures in financial statements.

- Simple errors like transposing numbers, miscalculating totals, or entering wrong figures into templates are a major source of mistakes.

- Rushing through assignments can cause overlooked errors or incomplete financial reports.

- Failing to double-check calculations or verify numbers with source documents often results in discrepancies.

- Financial reporting assignments often involve multiple steps, including journal entries, adjusting entries, and reconciliations, and missing any step can cause a chain of errors.

- Ignoring accounting standards such as IFRS or GAAP, even unintentionally, can make your report technically incorrect.

Understanding these reasons is the first step toward improving your accuracy and producing high-quality financial reporting assignments.

List of Common Errors in Financial Reporting Assignments

Certain mistakes keep appearing in financial reporting assignments. If you know what they are, then you can avoid making them.

- When you put a transaction in the wrong account, like listing a long-term debt as a current liability, your financial statements will be inaccurate.

- Forgetting to include transactions or items such as accrued expenses or unearned revenue can cause mistakes in your reports.

- Calculation mistakes in addition, subtraction, or percentages can give a wrong picture of your company’s financial performance.

- Forgetting to record adjustments for entries like depreciation, bad debts, or prepaid expenses can make your net income or asset values incorrect.

- Using different formats or accounting methods across your financial statements can confuse readers and make your work look unreliable.

- Not providing clear explanations or notes for your financial statements can make it hard for others to understand the numbers.

- Repeating mistakes from previous assignments or periods can lead to bigger inaccuracies over time.

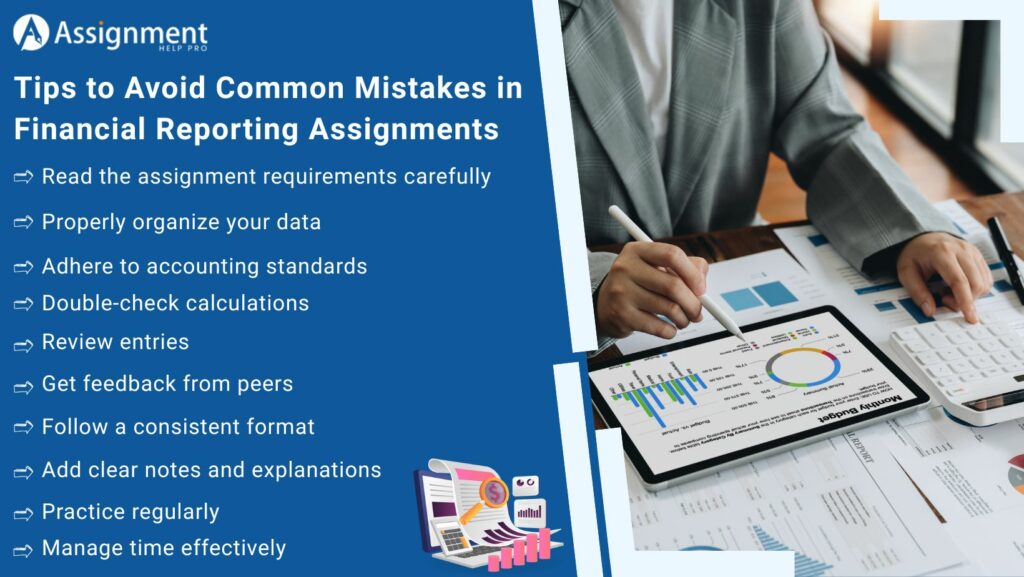

Tips to Avoid Common Mistakes in Financial Reporting Assignments

If you wish to avoid mistakes in your financial reporting assignments, then you need to follow a clear and organized approach. These are some practical financial report writing tips that will help you stay accurate

Read the assignment requirements carefully

Start by reading the instructions carefully so you know which financial statements, accounting rules, and reporting standards you need to follow. Ask your teacher or mentor if anything is unclear before you begin.

Properly organize your data

Keep all your transactions, documents, and journal entries well organized. Generally, using spreadsheets or accounting software can make managing your data much easier.

Adhere to accounting standards

Follow the correct accounting rules, like GAAP or IFRS. Keep guides nearby for complex transactions such as leases, revenue recognition, or currency conversions.

Double-check calculations

Use a calculator, spreadsheet formulas, or accounting tools to double-check all totals, subtotals, and percentages. Even a small mistake can affect your final report.

Review entries

Ensure that your journal entries are balanced, your reconciliations are in sync with the bank statements, and adjustments are posted properly. Also, check whether assets equal liabilities plus equity on the balance sheet.

Get feedback from peers

Talk about your work with classmates. Otherwise, get professional finance assignment help or accounting assignment help. This can give you a new perspective and help spot mistakes you might have missed.

Follow a consistent format

Format your financial statements professionally and consistently. Typically, using the same layout and terms throughout will make your financial report easier to read and help you avoid mistakes.

Add clear notes and explanations

Clearly explain your assumptions, methods, and major account changes. Adding these notes will increase the transparency of your work and reduce the chance of misinterpretation.

Practice regularly

Practicing financial reporting regularly will help you understand the concepts better and make fewer mistakes. It also boosts your confidence in handling assignments on your own.

Manage time effectively

Don’t wait until the last minute to submit your financial reporting assignment. Giving yourself enough time to review and fix mistakes will greatly improve your accuracy.

By following these strategies, you can reduce mistakes and create high-quality financial reporting assignments that show your skills and analytical ability.

Conclusion

Financial reporting is an important part of both your studies and professional accounting work. Accurate financial reporting is not just about numbers; it is about showing a clear and honest picture of a company’s financial health. Mistakes in financial reporting assignments are common, but you can prevent most of them by following the practical strategies and tips suggested in this blog. If you are still unsure how to fix or avoid errors in your financial reporting assignments, call us quickly. We have accounting and finance experts in our team to offer you customized assignment help online. Especially with their guidance, you can submit accurate financial reporting assignments on time and achieve the expected outcome.

FAQs

1. What are the most common mistakes in financial reporting assignments?

The most common mistakes are putting transactions in the wrong accounts and making calculation errors, as these directly affect the accuracy of your financial statements.

2. Can using accounting software reduce errors in financial reports?

Yes, tools like Excel, QuickBooks, or Tally can handle calculations and keep your work consistent. But you still need to check your entries and make sure everything is classified correctly.

3. How important are adjusting entries in financial reporting?

Adjusting entries are very important to report revenue, expenses, and assets correctly. But skipping them can make your financial results look higher or lower than they really are.

4. How can I prevent calculation errors in financial reports?

You can avoid mistakes by carefully checking your work, using spreadsheet formulas, and reviewing all totals step by step.